Financial-ML:

Predict S&P 500 Outperformers with ML

A machine learning system for equity selection that predicts which S&P stocks will outperform the market benchmark. The project combines market data, company fundamentals and sentiment indicators to construct long-only portfolios, using through a rigorous ML pipeline: data ingestion → feature engineering → expanding-window cross-validation → portfolio construction → comprehensive backtesting against SPY.

Key Results

| Metric | Value |

|---|---|

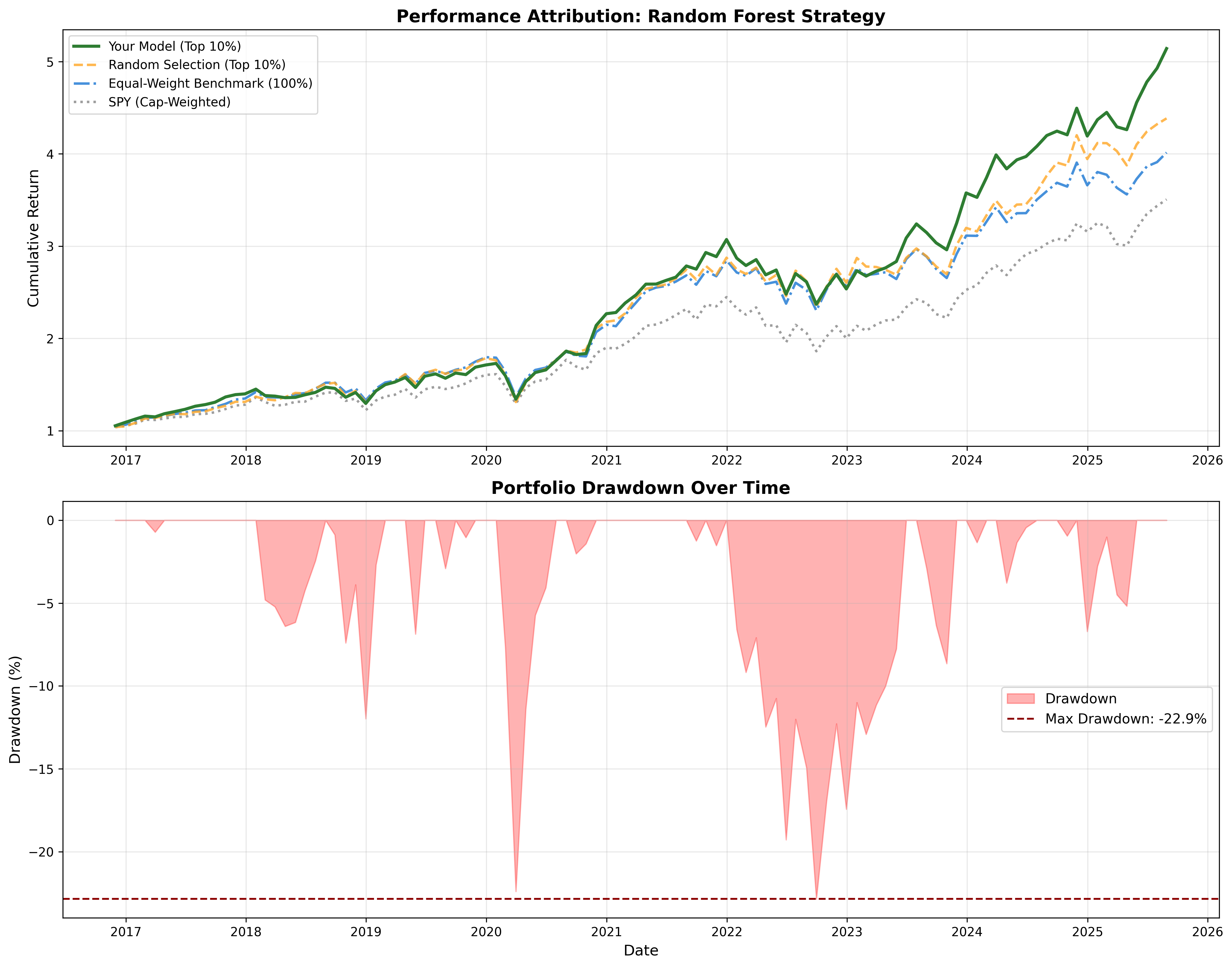

| Sharpe Ratio | 0.93 |

| Annual Return | 20.2% |

| Max Drawdown | -22.9% |

| Alpha vs Random | 1.72% |

| Win Rate | 69.8% |

- 100% Long-Only Strategy: Top 10% stocks, equal-weighted, monthly rebalancing

- Transaction costs included: 10 bps per trade, ~0.5% annual drag from 42% turnover

- Regime awareness: VIX-based features improve downside protection during volatile periods

- Statistically significant: Sharpe ratio outperformance (p < 0.001, Bonferroni-adjusted)

Data & Features

| Data Source | Features | Purpose |

|---|---|---|

| Market Data Yahoo Finance |

r12 (12m return) mom121 (momentum) vol3, vol12 (volatility) |

Momentum and risk regime signals |

| Fundamentals SEC EDGAR |

BookToMarket ROE, ROA, NetMargin Leverage, Asset Growth, Net Share Issuance |

Value, quality, and financial health |

| Sentiment VIX Index |

VIX percentile (12-month rolling) | Market stress detection |

Models Evaluated

- Logistic Regression: Simple baseline for comparison

- Random Forest: Selected for production—balances accuracy with stable predictions

- Gradient Boosting & XGBoost: Tested but tend to overfit in market prediction tasks

Why Random Forest won: It maintains a wider range of confidence scores, making it better at ranking stocks. Boosting methods were too aggressive and didn't improve results.

How It Works

The Pipeline

- Collect Data: Download market prices (Yahoo Finance), fundamentals from SEC filings, and VIX sentiment

- Engineer Features: Extract 13 features from the data (momentum, volatility, value ratios, regime indicators)

- Train Model: Use 15 years of historical data with time series cross-validation to prevent overfitting

- Generate Predictions: Random Forest model predicts which stocks will outperform S&P 500 next month

- Construct Portfolio: Select top 10% highest-confidence stocks, equally weight, rebalance monthly

- Validate Results: Backtest against S&P 500 benchmark with real transaction costs

Model Validation

The model uses expanding-window time series cross-validation, where each month's predictions are tested on future data the model has never seen. This prevents overfitting and mimics real-world deployment.

Quick Start

Installation

git clone https://github.com/pmatorras/financial-ml.git

cd financial-ml

python -m venv .venv

source .venv/bin/activate

pip install -e .Run Full Pipeline

make data # Collect market, fundamentals, sentiment

make train # Train models

make backtest # Analyze and backtestQuick Test

make test # Run pipeline on subset with debug mode

For advanced usage, flags, and development modes, see the

GitHub repository